Bussiness

The New York Times Company’s Subscription Revenues Fuel Growth

In today’s fast-evolving media landscape, where adaptability and digital innovation are key, The New York Times Company NYT has set itself apart through strategic transformations and a growing subscriber base. While many traditional media companies have struggled, NYT has thrived by focusing on diversifying revenue streams, optimizing costs and adapting to shifting consumer preferences. The company’s emphasis on bundled subscriptions reflects a smart approach to capturing evolving reader interests.

By embracing technology, The New York Times Company has deepened its connection with its audience. Strategic acquisitions like Wirecutter and The Athletic have expanded its reach, allowing it to tap into new markets. These moves demonstrate NYT’s agility and commitment to staying relevant in an increasingly competitive media environment.

NYT’s Subscription Revenues: A Growth Engine

The New York Times Company’s growing subscriber base is a central pillar of its success. With the increase in subscribers, the company enhances its influence and appeal, attracting advertisers keen on reaching a broad, engaged audience.

At the close of the second quarter of 2024, The New York Times Company had approximately 10.84 million subscribers across its print and digital offerings. Of this total, 10.21 million were digital-only subscribers, including around 4.83 million bundle and multiproduct subscribers. Compared to the preceding quarter, the company added 300,000 net new digital-only subscribers, underscoring its steady growth trajectory.

Subscription revenues of $439.3 million grew 7.3% year over year. Subscription revenues from digital-only products jumped 12.9% to $304.5 million. This reflects an increase in bundle and multiproduct revenues and a rise in other single-product subscription revenues.

The company has also seen consistent improvement in its digital-only average revenue per user (ARPU), which rose to $9.34 in the second quarter compared to $9.15 in the same period last year. This growth in ARPU is largely driven by subscribers transitioning from promotional pricing to regular rates, along with price increases for long-term, non-bundle subscribers.

The New York Times Company expects further gains in subscription revenues in the third quarter of 2024. Management projects overall subscription revenues to grow by 7-9%, with digital-only subscription revenues forecasted to increase by 12-15%, signaling continued momentum in its digital business.

Image Source: Zacks Investment Research

NYT: In a Nutshell

The New York Times Company’s strategic focus on subscription growth and digital innovation has proven to be a key driver of its success in a competitive media landscape. Its ability to consistently expand its digital offerings, attract new subscribers and optimize ARPU showcases its resilience and strong market positioning. For investors, NYT’s growth trajectory, bolstered by its digital strategy and increasing subscription revenues, signals that the company is well-positioned for sustained success.

As it continues to adapt to technological advances and changing reader preferences, The New York Times Company remains an attractive investment opportunity sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

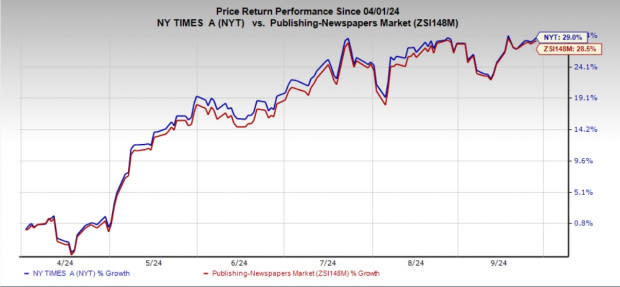

Shares of The New York Times Company have risen 29% in the past six months compared with the industry’s growth of 28.5%.

Other Stocks Worth Looking

Here, we have highlighted three other top-ranked stocks, namely Aspen Technology AZPN, PayPal Holdings PYPL and Datadog DDOG.

Aspen Technology, a global leader in industrial software, currently sports a Zacks Rank #1. AZPN has a trailing four-quarter average earnings surprise of 4.2%.

The Zacks Consensus Estimate for Aspen Technology’s current financial-year sales and earnings suggests growth of 5.5% and 12.8%, respectively, from the year-ago reported numbers.

PayPal Holdings, a global digital payments platform, currently sports a Zacks Rank #1. PYPL has a trailing four-quarter average earnings surprise of 14%.

The Zacks Consensus Estimate for PayPal Holdings’ current financial-year sales suggests growth of 7.3% from the year-ago reported numbers.

Datadog, the monitoring and security platform for cloud applications, currently carries a Zacks Rank #2 (Buy). DDOG has a trailing four-quarter average earnings surprise of 21.7%.

The Zacks Consensus Estimate for Datadog’s current financial-year sales and earnings suggests growth of 23.4% and 23.5%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The New York Times Company (NYT) : Free Stock Analysis Report

Aspen Technology, Inc. (AZPN) : Free Stock Analysis Report

PayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report

Datadog, Inc. (DDOG) : Free Stock Analysis Report

Report: Knicks sign Landry Shamet

Knicks bringing back veteran guard Landry Shamet

Knicks Bring Back Landry Shamet

Giants disaster: Two-time Super Bowl champion says ‘everyone must go’ in New York after 10th straight loss

2024 NFL season, Week 16: What We Learned from Sunday’s games

New York City police investigate death of woman found on fire in subway car

New York Knicks Make Roster Move Before Raptors Game

Falcons Blowout Giants in Michael Penix’s First Start: 3 Takeaways

Michael Penix Jr. Excites NFL Fans as Falcons Beat Giants After Kirk Cousins Benched